Table of Contents

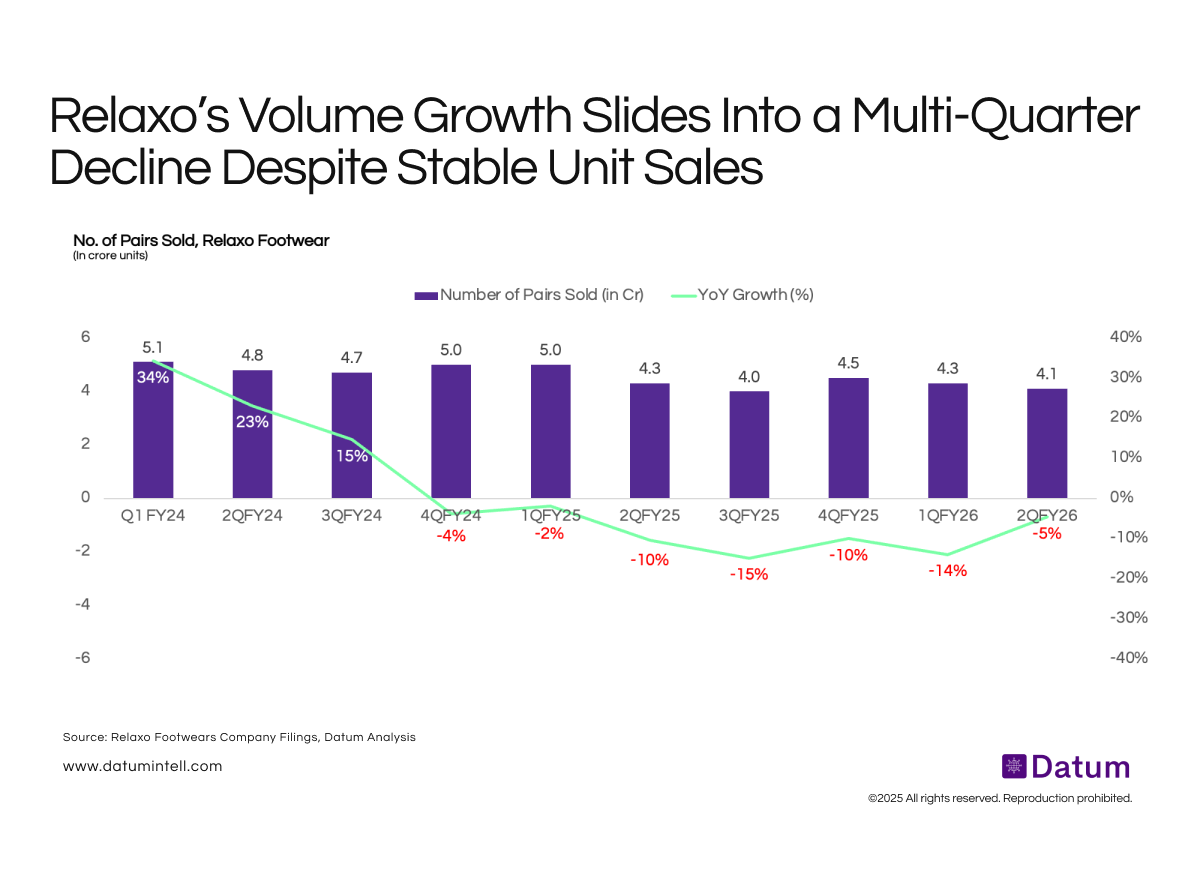

Relaxo’s volume trajectory has deteriorated steadily since late FY24, moving from high double-digit growth to consistent YoY declines of –2% to –15%. In 2Q FY26, the company also reported a sharp 7.5% YoY revenue decline, driven by demand softness in the mass segment and delayed purchases ahead of GST 2.0 implementation. General trade remained muted, with distributors clearing legacy inventory rather than placing fresh orders. Realisations fell 3% YoY to ₹151 per pair, although EBITDA margins held firm at 12.9%, supported by operational efficiencies and tight cost control. Management expects this weakness to be temporary, with demand normalising as GST-adjusted inventory reaches the market.

What It Means

Relaxo’s sustained negative YoY volume prints indicate that the company is facing a structural slowdown at the bottom of the pyramid, where consumption recovery remains fragile. The GST transition-created pause in channel stocking exacerbated existing weakness, masking underlying stabilisation in absolute volume levels (~4–4.5 crore pairs per quarter). While short-term pressure is likely to persist, management’s expectation of sequential improvement over the next 2–3 quarters-driven by distribution expansion, sales transformation, and clearer channel pipelines—suggests a potential gradual return to volume-led growth. Margin resilience amid softer realisations provides some cushion, but a healthy recovery hinges on a revival in mass-market demand and effective execution of the new distribution strategy.

{kind=link}