Table of Contents

In our earlier post, The Power of Few: How Just 18% of Brands Drive 80% of Blinkit’s Sales, we outlined a striking Pareto dynamic in Blinkit’s marketplace — a small set of brands account for the lion’s share of sales. This raised a critical follow-up question: who are these top-performing brands, and what role do D2C players play within them?

New data sheds light on this question by dissecting the composition of top brands, specifically examining the split between Direct-to-Consumer (D2C) and Traditional brands. The findings offer sharp strategic implications for both incumbents and emerging digital-first players.

The 80% Sales Pie: Still Largely Traditional, But D2C Is Rising

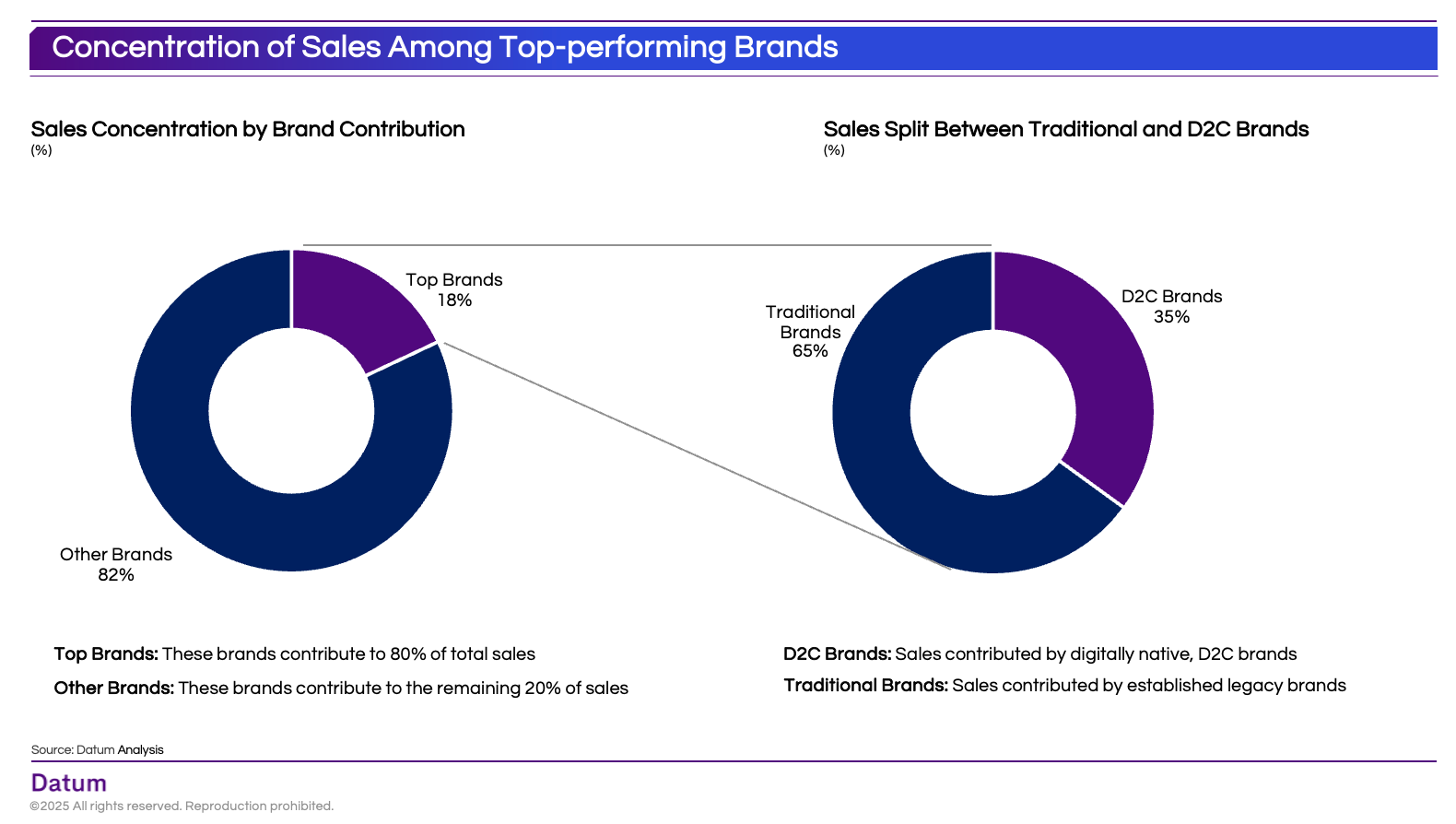

Among the brands contributing to 80% of Blinkit’s sales, a majority (65%) are traditional legacy brands. These are players with long-established offline distribution and brand recall. However, D2C brands — accounting for 35% — are making meaningful inroads, especially in premium, gifting, and niche categories.

In the donut breakdown, while only 18% of all brands drive 80% of sales, over a third of these elite contributors are D2C — signaling a quiet but potent disruption.

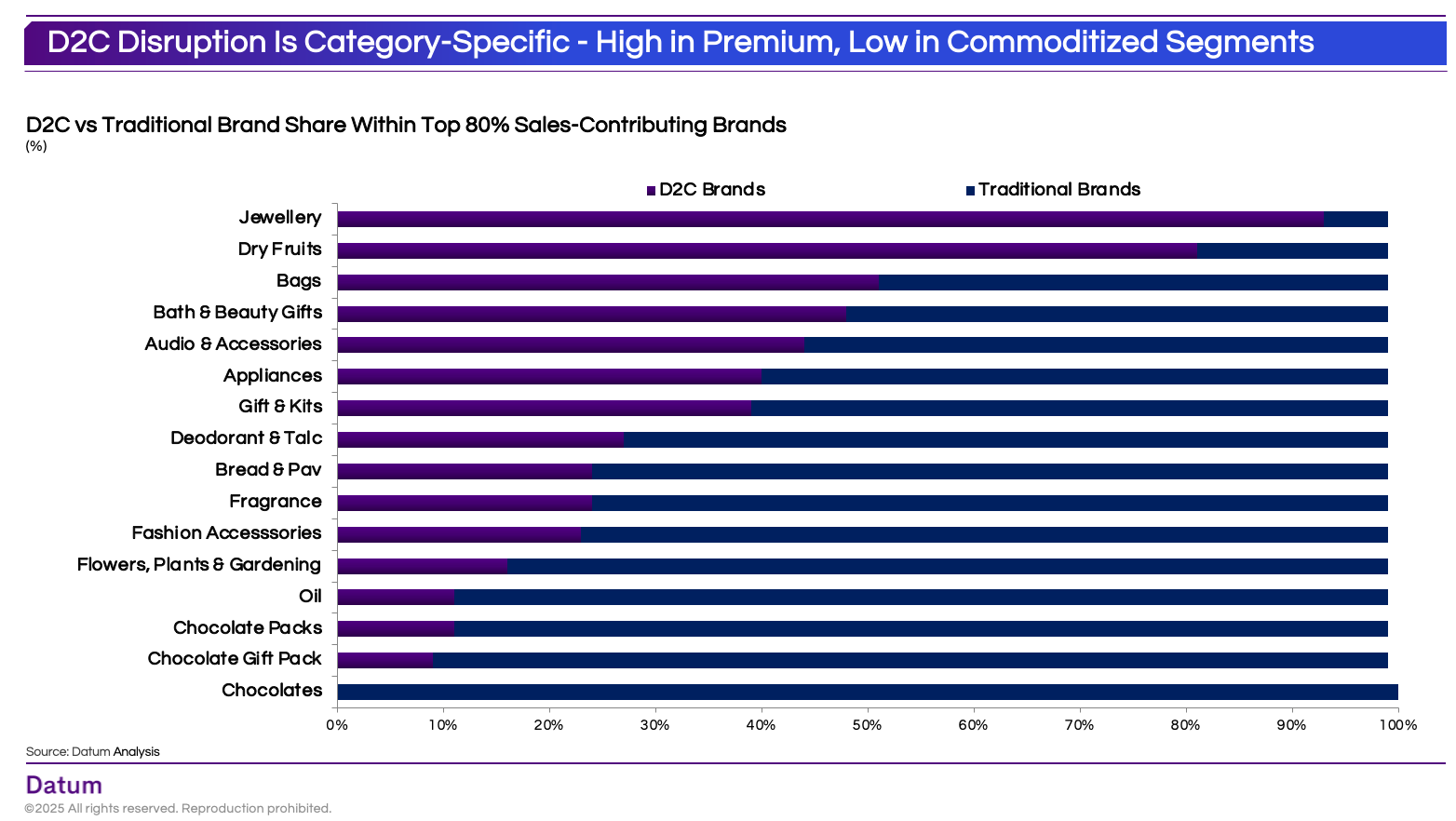

D2C Disruption Is Category-Specific — High in Premium, Low in Staples

A deeper look at category-wise contribution reveals a clear pattern. D2C brands have captured significant share in premium, experiential, and giftable categories.

- D2C Dominates in Select Gifting and Premium Categories. Categories like Jewellery, Dry Fruits, Bags, and Bath & Beauty Gifts show strong D2C penetration (30–50%), highlighting consumer openness to digital-first brands in high-margin or giftable segments.

- Traditional Brands Retain Dominance in Daily-Use and Commodity Categories. In categories such as Oil, Chocolates, Chocolate Packs, and Deodorant & Talc, D2C brands contribute less than 20%, reinforcing the entrenched position of legacy players where brand familiarity and distribution scale matter.

- Emerging Opportunities in Bread & Pav, Fragrance, and Fashion Accessories. D2C presence in Bread & Pav, Fragrance, and Fashion Accessories (20–30%) signals evolving consumer willingness to explore niche, experience-led D2C offerings, even in low-ticket, high-frequency segments.

- White Space in Low-Involvement Categories. Categories like Chocolates and Chocolate Gift Packs remain largely untapped by D2C brands, representing a growth opportunity for digital disruptors to innovate in packaging, personalization, or bundling.

- Gifting & Seasonal Categories Prime for D2C Acceleration. High D2C share in Gift & Kits, Bags, and Bath & Beauty Gifts reflects consumer preference for curated, aesthetically packaged products — a strength of D2C brands. Continued focus on brand storytelling and convenience could expand market share further.

In some of these, D2C players contribute nearly half the sales — a remarkable feat considering their relatively recent entry into the market.

Conversely, commoditized and habit-driven categories such as Chocolates, Oils, Bread & Pav, and Deodorants remain largely dominated by traditional players.

D2C brands win where packaging, storytelling, and discovery matter. Traditional brands win where familiarity, price, and consistency dominate consumer choice.

Implications for Category Strategy and Brand Playbooks

- Quick Commerce Players like Blinkit can capitalize on this duality by curating premium D2C assortments in emerging gifting and wellness verticals while optimizing core selection in staples with high-velocity traditional brands.

- Traditional FMCG brands must rethink innovation pipelines to counter D2C players’ agility, especially in high-margin categories like personal care and niche food.

- D2C brands must balance scale with focus — doubling down on high-performing categories while resisting the temptation to overextend into low-D2C-fit segments.

While legacy brands still rule Blinkit’s topline, D2C brands are punching above their weight — not just in share of sales, but in shaping consumer perceptions and future growth pockets.

This shift echoes a broader truth in Indian e-commerce: the future may still be built on the shoulders of giants, but it is increasingly being painted by the challengers.

If you’re a brand looking to crack Quick Commerce, let’s talk. Write to us at hello@datumintell.com if you have any questions, inquiries, or collaboration opportunities. We’d love to hear from you!

{kind=link}